Financial Planning

The purpose of a financial plan is to create a comprehensive roadmap for achieving your financial goals and effectively managing your resources. It helps you define both short-term and long-term objectives, such as building an emergency fund, saving for retirement or purchasing a home.

A financial plan outlines a budget that tracks income, expenses, and savings, enabling you to manage cash flow and make informed spending decisions. It can help establish a tailored investment strategy aligned with your risk tolerance and financial aspirations, while also addressing potential risks through insurance and diversification. The plan considers tax implications to help minimize liabilities, ensuring you retain more of your earnings. It also includes retirement planning, outlining steps to secure your desired lifestyle, and estate planning to guide the management and distribution of your assets after your passing.

Ultimately, a financial plan serves as a benchmark for tracking progress and adjusting strategies, fostering accountability in achieving your financial objectives. During the planning process, I focus on establishing four core metrics to guide your investment structure moving forward, empowering you to make informed decisions and work towards financial security and independence. These core metrics are your financial goals, your investment time horizon for each account, your capacity for loss and your cognitive risk tolerance.

Financial goal setting

Setting financial goals is essential for several reasons. First and foremost, these goals provide clear direction and focus for the financial decisions you make. When you know what you’re aiming for, it becomes easier to prioritise your spending and saving. Goals could be in the form of spending a specific amount during your retirement, leaving a certain amount to your children or purchasing that dream home in the next 5 years.

Having specific goals can be a powerful source of motivation. They inspire you to stay committed to your plans, making it easier to adhere to a budget, savings or gifting strategy. As you work towards these goals, you can track your progress over time, with the flexibility to make adjustments when necessary.

In essence, setting financial goals is a vital step towards achieving financial security and success, guiding your decisions and actions as you work toward your desired outcomes.

Required rate of investment return

Calculating your required rate of investment return to achieve your financial goals is crucial and ultimately shapes your financial strategy. This rate acts as a benchmark for your investment decisions, guiding you towards achieving your specific goals. Whether you’re saving for retirement, a major purchase, or your children’s education, knowing the return you need helps you identify appropriate investment vehicles and strategies.

Additionally, understanding your required rate of return in a contributing factor when assessing your risk tolerance. Investments with higher potential returns often come with increased risk, so having a clear target helps you determine how much risk you’re willing to take on. This understanding ensures that your investment choices align with your comfort level, which is vital for maintaining your portfolio.

This rate informs your asset allocation strategy. Different asset classes have varying historical returns and risk profiles. Knowing your required return helps you construct a diversified portfolio that aims to meet your goals while managing risk effectively.

Investment time horizon

Establishing your investment time horizon is crucial because it serves as a foundational element in shaping your overall investment strategy. Your time horizon, essentially the length of time you plan to hold an investment before needing to access the funds, directly influences several key decisions.

A clearly defined time horizon helps you determine the appropriate level of risk you can take. If you’re investing for a long-term goal, such as retirement in 20 or 30 years, you can generally afford to take on more risk, as you have time to ride out market fluctuations. Conversely, if your goal is short-term, like saving for a house deposit in a few years, you’ll want a more conservative approach to protect your capital from potential losses.

Your time horizon influences the types of investments that are suitable for your portfolio. Longer time horizons often allow for a greater allocation to equities, which have historically offered higher returns over extended periods. In contrast, shorter time horizons might necessitate a focus on more stable investments, such as bonds or cash equivalents, which can provide liquidity and lower volatility.

Future cashflow analysis

Using advanced financial planning software, I can analyse your income and outgoings over the course of your lifetime to establish if there are any short-term bottlenecks or long-term cash flow shortfalls. This analysis is particularly useful when deciding if you should gift assets to children, retire early or adjust your spending patterns.

By visualising your financial trajectory, I can pinpoint critical moments when your cash flow might be strained, allowing us to strategise effectively. For example, if the analysis reveals a potential shortfall during a significant life event, such as funding education for your children or making a major purchase, we can explore options to adjust your savings or investment strategies accordingly.

If you’re contemplating early retirement, the software allows us to simulate various scenarios, assessing how your lifestyle choices and spending will affect your long-term financial health. This means we can create a plan together that balances your desire for leisure and fulfilment with the financial realities of retirement.

Cognitive risk tolerance

Understanding the amount of volatility you are cognitively comfortable with allows me to assess the suitability of various risk levels from the perspective of your behavioural bias. Ultimately, the goal of this exercise is to ascertain if you would be comfortable with what I expect the volatility to be in various portfolios. If, for example, a portfolio fell by 20% I want to ensure that those cognitive bias’ don’t create wealth destruction by leading you to make the decision to sell the investments at the trough (or near enough) of their correction.

Defined, cognitive risk tolerance refers to an individual's ability to understand, evaluate, and manage risks based on their cognitive capacities. It encompasses how a person perceives risk, processes information about potential outcomes, and makes decisions in uncertain situations. Factors influencing cognitive risk tolerance include prior knowledge, experience, emotional responses, and cognitive biases. Higher cognitive risk tolerance generally means a greater willingness to engage in riskier decisions, while lower tolerance may lead to more conservative choices.

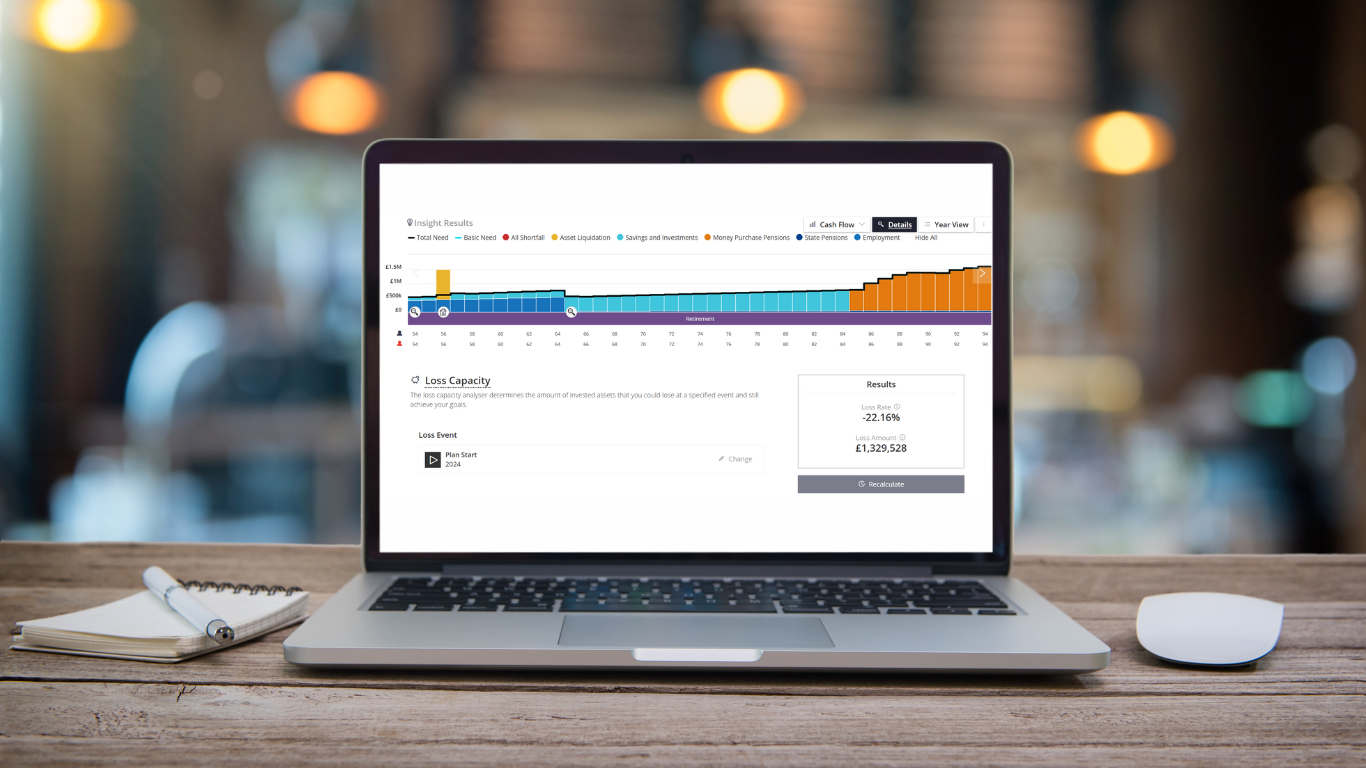

Loss capacity

I assess loss capacity to identify the extent to which a plan can sustain losses from investments and pensions during a specific event while still meeting its objectives. This is usually an objective percentage, and can be referenced against an allocations previous maximum drawdown to assess the suitability of that risk budget in the first instance.

I analyse this figure with major loss scenarios, which are designed to model various degrees of market downturns. Based on the severity of the correction, this insight generates an output that indicates the minimum investment return needed to prevent shortfalls, if any. The major loss event can be used to model the integration of a market correction as a lasting element in a client's financial plan.

The cashflow planning software I use also provides insights in to the effect a less permanent market crash would have on your financial future, assessing the volatility of a portfolio with a similar risk budget encountered during previous financial crashes to see if this impacts your plan.